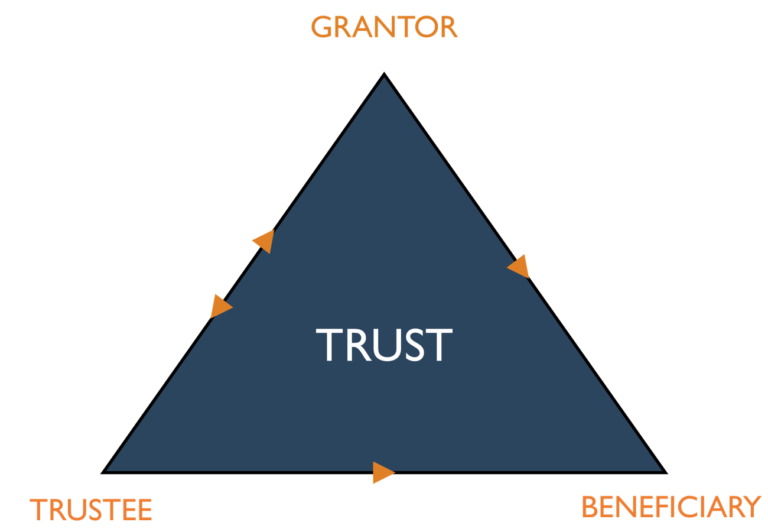

A Trust is an Agreement between Grantor and a Trustee to hold Assets which may be personal family assets as well as businesses and investments assets for a the benefit of specified Beneficiaries in accordance with the terms of trust agreement.

New trust reporting requirements

Trusts are a powerful tool used in tax and financial planning. The main advantage of a trust is that it allows you to separate the control and management of assets in the trust from its ownership. Trusts have many uses in both family and estate planning and as a tool to administer an estate on the death of an individual.

In order to increase the transparency of how trusts are used, and on the persons who have created, control and benefit from trusts, the federal government announced new trust reporting rules in its 2018 budget to improve the collection of this information.. The new requirements are a considerable change from the current rules and carry significant penalties for non-compliance. Trustees of affected trusts need to understand the new reporting obligations, assess whether the required information is readily available, and plan to obtain the necessary details to ensure compliance. Draft legislation released on February 4, 2022 announced that the new rules will apply for trust taxation years ending on or after December 31, 2022 (they were originally proposed to apply for taxation years ending on or after December 31, 2021.

The current rules

In the current environment, a trust generally has to file a T3 annual return if it has taxes payable or makes a distribution to one or more beneficiaries. Personal information on trustees, beneficiaries, settlors or other persons are not currently required to be reported to the Canada Revenue Agency (CRA).

The new rules For trust taxation years ending on or after December 31, 2022, all non-resident trusts that currently have to file a T3 return and express trusts that are resident in Canada, with certain exceptions, will be required to report additional information as part of their T3 return each year. The draft legislation indicates that bare trusts (generally, where the trustee can reasonably be considered to act as an agent for the beneficiaries) will be subject to the new requirements.

New filing requirement

With limited exceptions, the new rules generally require the filing of a T3 return by express trusts that are resident in Canada even if it does not have any income to report. An express trust is generally a trust created with the settlor’s express intent, such as through a trust deed or a will, as opposed to a resulting or constructive trust, or certain trusts deemed to arise under the provisions of a statute. This includes trusts such as those created to hold private company shares as part of an estate freeze, and trusts created to hold vacation or other personal property.

Enhanced reporting obligation

Each year, affected trusts must report additional information on all trustees, beneficiaries, settlors, and each person who has the ability to exert control or override trustee decisions over the appointment of income or capital of the trust (e.g., a protector), including:

- Name

- Address

- Date of birth

- Jurisdiction of residence

- Taxpayer identification number, such as social insurance number, trust account number, business number or taxpayer identification number used in a foreign jurisdiction

This enhanced reporting obligation aims to help the government more effectively counter aggressive tax avoidance, tax evasion, money laundering, and other criminal activities perpetrated through the misuse of trusts. With this in mind, trustees should know that reporting this new information may prove onerous for certain trusts and should plan ahead to be in compliance.

This information should be reported on a new schedule to be filed with the trusts T3 return. Note that affected trusts must file the T3, including the new schedule, and cannot simply file the new schedule on its own even if the trust has no income for the year. In the case of family trusts, this means that they will need to be transparent with respect to all possible beneficiaries, even contingent beneficiaries, of the trust, as well as making annual trust filings in years where there is no distribution of income or capital.

Exceptions

There are exceptions to the new reporting requirements, including:

- Trusts that have been in existence for less than three months

- Trusts that hold assets not exceeding $50,000 in total fair market value throughout the year (where the only assets are cash, certain government debt obligations, a share, debt or right listed on a designated stock exchange, a share of a mutual fund corporation, a unit of a mutual fund trust, and an interest in a related segregated fund)

- Certain regulated trusts, such as a lawyer’s general trust account

- Trusts that qualify as non-profit organizations or registered charities

- Mutual fund trusts, segregated funds, and master trusts

- Graduated rate estates

- Qualified disability trusts

- Employee life and health trusts

- Certain government funded trusts

- Trusts under or governed by certain registered plans

- Cemetery care trusts and trusts governed by eligible funeral arrangements

Penalties

New penalties are being introduced along with the new reporting requirements. With respect to the new reporting obligations, if any person or partnership knowingly or under circumstances amounting to gross negligence makes a false statement or omission in the return of a trust, fails to file a return for a trust, or fails to comply with a demand to file a return, the penalty is the greater of:

- $2,500

- 5% of the highest total fair market value of all the property held by the trust in the year

For affected trusts that hold high value assets, such as a vacation home or shares of a private corporation, the cost of non-compliance can be significant.

In addition, existing penalties in respect of T3 returns continue to apply. The penalty for the failure to file a T3 return is $25 per day with a minimum of $100, and can increase up to $2,500.

CRA modernizing T3 trust return processes

In anticipation of the increase in volume of T3 returns that will be filed because of the new rules, the CRA is modernizing its systems and processes used for T3 returns. Planned changes will be rolled out over the next few years, beginning with online registration for trust account numbers in CRA’s My Business Account service in 2021. The CRA is planning to introduce T3 electronic filing for certain T3 return types in 2022 and electronic filing will be available for all other T3 return types in 2023.

When the CRA has the capability to receive and process T3 returns electronically, it will be much more equipped to analyze and assess T3 information, including the new beneficial ownership details required to be reported. Taxpayers should get used to the increased transparency with respect to trusts, which will likely come with heightened scrutiny from the CRA.